Justin

Justin

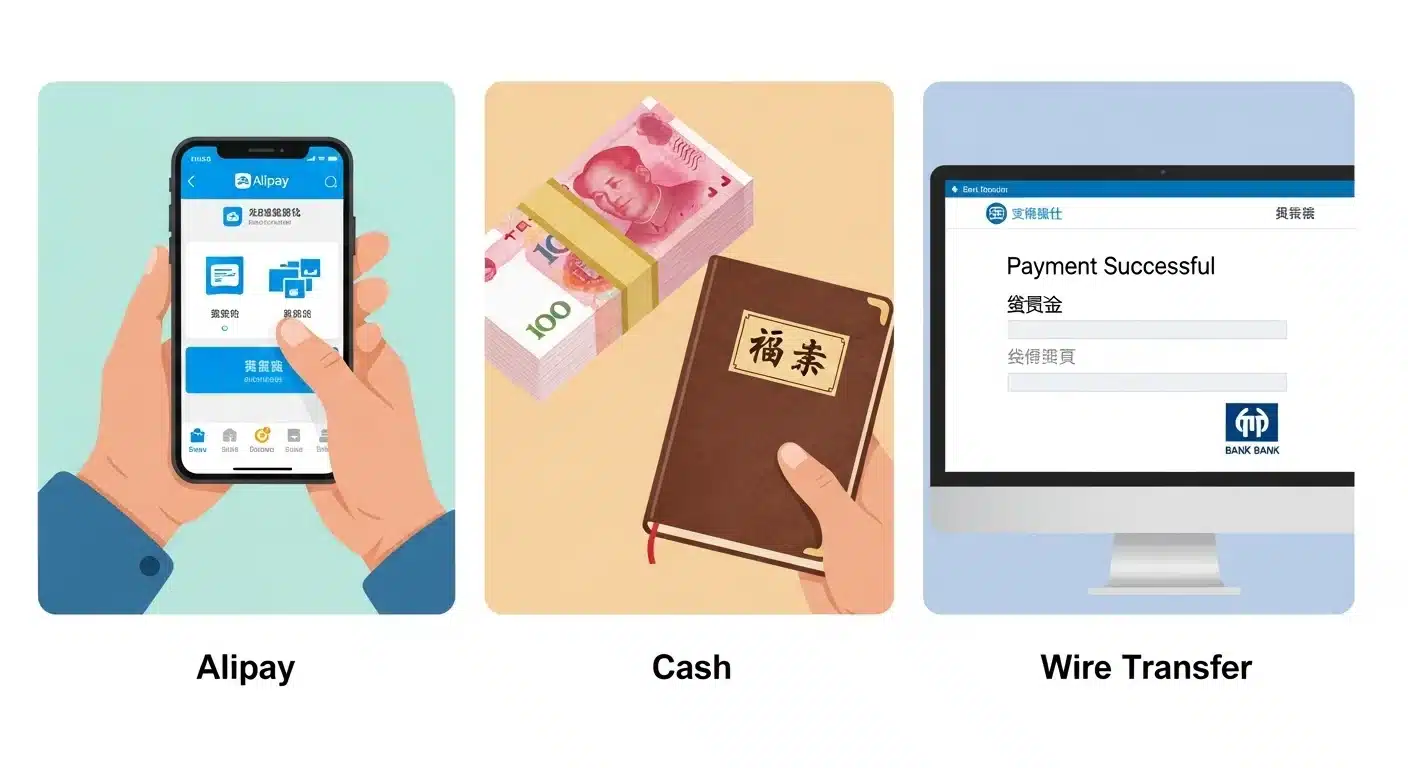

Navigating supplier payments in Yiwu can be a major bottleneck for importers. Choosing the wrong method can lead to frozen transactions, hit strict spending caps, or leave you with no recourse in a dispute.

This guide breaks down the practical realities of paying suppliers in Yiwu. We compare the limits, risks, and best uses for bank transfers (T/T), Alipay, and cash, using specific data like the 3% cross-border fee on WeChat Pay and the $50,000 annual cap on foreign-linked Alipay accounts to help you make a secure, cost-effective choice.

Industry Manufacturers List

Quick Comparison: Top Picks

| Manufacturer | Location | Core Strength | Verdict |

|---|---|---|---|

| Apple Pay | Global Standard | Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption. | A top-tier digital wallet using tokenization and biometrics for secure, convenient payments across devices. |

| Google Pay | Global Standard | Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption. | A versatile digital wallet offering secure tokenized payments and seamless checkout across Android and web platforms. |

| PayPal | Global Standard | Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption. | A widely accepted digital wallet and payment platform known for buyer protection and easy online transactions. |

| Samsung Pay | Global Standard | Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption. | A Samsung device-centric wallet praised for its MST technology compatibility and strong security features. |

| Venmo | Global Standard | Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption. | A social payments app popular for peer-to-peer transfers, expanding into merchant payments with secure tokenization. |

| EMV Chip & Contactless Card Payments | Global Standard | EMV chip card transactions, NFC contactless card payments, point‑to‑point encryption from card reader to processor, and fraud‑liability reduction versus magstripe. | The global standard for secure in-person payments, using dynamic cryptograms to drastically reduce cloning fraud. |

| Open Banking & Direct Bank Transfers (ACH / Account-to-Account) | Global Standard | API‑initiated bank payments, ACH / SEPA / faster‑payments transfers, strong customer authentication, and real‑time account verification instead of card PAN use. | A secure alternative moving money directly between banks, minimizing card fraud and chargeback risks for high-value transactions. |

Apple Pay

Apple Pay is a digital wallet that stores encrypted card or bank details. It uses tokenization and biometric or device-based authentication to complete payments without exposing the underlying card number. By 2026, it is widely considered one of the safest consumer payment methods available.

Its security model is built on replacing sensitive data with unique tokens, storing them in a secure hardware element on the device, and requiring verification via fingerprint, Face ID, or a passcode before every transaction.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption.

- 🌍 Key Markets: In‑person contactless payments, ecommerce checkout, in‑app purchases, marketplaces, and peer‑to‑merchant transactions.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Google Pay

Google Pay is a digital wallet that stores encrypted card or bank details. It uses tokenization and biometric or device-based authentication to complete payments without exposing the underlying card number. By 2026, it is widely regarded as one of the safest consumer payment methods because sensitive data is replaced with tokens, protected in secure hardware elements, and verified via fingerprint, Face ID, or a passcode before each transaction.

The service operates on a global scale, providing a standardized payment infrastructure. Its core strength lies in processing tokenized card-on-file payments, enabling NFC tap-to-pay, and facilitating one-click checkout in apps and browsers, all secured by biometric authentication and device-level encryption.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption.

- 🌍 Key Markets: In‑person contactless payments, ecommerce checkout, in‑app purchases, marketplaces, and peer‑to‑merchant transactions.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

PayPal

PayPal is a digital wallet that stores encrypted card or bank details. It uses tokenization to replace sensitive data with secure tokens and completes payments using biometric or device-based authentication, like a fingerprint or Face ID, without exposing the underlying card number.

By 2026, it is widely considered one of the safest consumer payment methods. This reputation comes from its core approach: sensitive information is never directly shared during a transaction. Instead, tokens are used, protected in secure hardware elements, and each payment requires verification via a fingerprint, facial scan, or passcode.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption.

- 🌍 Key Markets: In‑person contactless payments, ecommerce checkout, in‑app purchases, marketplaces, and peer‑to‑merchant transactions.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Samsung Pay

Samsung Pay is a digital wallet that securely stores your card and bank information. It uses advanced encryption and a process called tokenization, which replaces your actual card number with a unique, one-time code for each transaction. This means your sensitive financial data is never directly shared with merchants, significantly reducing the risk of fraud.

The service is built on a foundation of robust security. Every payment is locked behind biometric verification—like your fingerprint or face scan—or a device passcode. This multi-layered approach, combined with storing data in a dedicated, tamper-resistant chip (a secure element), has made Samsung Pay one of the most trusted consumer payment methods available today.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption.

- 🌍 Key Markets: In‑person contactless payments, ecommerce checkout, in‑app purchases, marketplaces, and peer‑to‑merchant transactions.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Venmo

Venmo is a digital wallet that stores encrypted card or bank details. It uses tokenization and biometric or device-based authentication to complete payments without exposing the underlying card number. By 2026, it is widely regarded as one of the safest consumer payment methods because sensitive data is replaced with tokens, protected in secure elements, and verified via fingerprint, Face ID, or a passcode before each transaction.

Its production capacity is built around a secure, scalable platform that processes tokenized card-on-file payments, NFC tap-to-pay, and one-click checkout flows. The system is designed to handle high volumes of transactions across in-person, in-app, and online environments while maintaining stringent security protocols.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: Tokenized card-on-file payments, NFC tap‑to‑pay, in‑app and browser one‑click checkout with biometric authentication and device‑level encryption.

- 🌍 Key Markets: In‑person contactless payments, ecommerce checkout, in‑app purchases, marketplaces, and peer‑to‑merchant transactions.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

EMV Chip & Contactless Card Payments

EMV chip and tap‑to‑pay card transactions create dynamic, one‑time cryptograms for each purchase, making card data far harder to clone than traditional magnetic‑stripe swipes. When combined with PCI‑compliant terminals and point‑to‑point encryption, chip and contactless cards are considered one of the most secure in‑person card payment methods in 2026.

The system’s core strength lies in its ability to handle EMV chip card transactions and NFC contactless card payments, supported by point‑to‑point encryption from the card reader to the processor. This setup significantly reduces fraud liability compared to older magstripe technology.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: EMV chip card transactions, NFC contactless card payments, point‑to‑point encryption from card reader to processor, and fraud‑liability reduction versus magstripe.

- 🌍 Key Markets: Retail point‑of‑sale, restaurants, events and booths, and any card‑present environment requiring fast yet secure checkout.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Open Banking & Direct Bank Transfers (ACH / Account-to-Account)

Open banking and account-to-account transfers move money directly between bank accounts with strong bank-grade authentication, such as multi-factor and PSD2 SCA in many regions. This approach reduces reliance on card numbers that can be stolen or misused.

These methods significantly cut card-related fraud and chargeback risk. They are viewed as safer alternatives for high-ticket or recurring payments in 2026.

At a Glance:

- 📍 Location: Global Standard

- 🏭 Core Strength: API‑initiated bank payments, ACH / SEPA / faster‑payments transfers, strong customer authentication, and real‑time account verification instead of card PAN use.

- 🌍 Key Markets: B2B payments, subscriptions and invoices, high‑value ecommerce, payouts, and platforms seeking lower fraud and chargeback exposure.

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Can I Pay with US Dollars Cash?

In most in-person retail settings in the United States you can still pay with physical US dollar cash, but not all merchants accept it, and acceptance is declining. Federal Reserve and industry data show that cash accounts for roughly 11–16% of in-person consumer transactions, and only about 60% of US businesses still accept cash at all. Small, temporary, or card-centric vendors (like booths) may choose to be “card-only” or “cashless,” so you must check the specific booth’s posted policy or ask the operator directly.

Cash Acceptance in the US Market

Physical US dollar cash is still a valid payment method in many in-person retail settings.

However, acceptance is not universal and is declining across the country.

The decision to accept cash is up to each individual merchant or booth operator.

The Reality of a Cashless Trend

Federal Reserve and industry data indicate cash is used for only 11–16% of in-person consumer transactions.

Roughly 60% of US businesses currently accept cash, meaning a significant portion are cashless.

Small, temporary, or card-focused vendors, such as market booths, are more likely to be ‘card-only’.

Always check a vendor’s posted payment policy or ask directly before assuming cash is accepted.

WeChat Pay & Alipay: Limits for Foreigners

Foreign visitors can link international cards to Alipay and WeChat Pay for everyday spending, but face strict transaction and annual caps, and cannot use these accounts for peer-to-peer transfers to personal accounts.

How the Systems Work for Foreigners

Foreign visitors can link Visa, Mastercard, or other international cards directly to Alipay and WeChat Pay without needing a Chinese bank account.

This setup allows you to pay merchants via QR codes for everyday expenses, shopping, and dining.

However, these accounts are designed for consumption, not business transfers. Features like peer-to-peer (P2P) payments to personal accounts are typically restricted or blocked for foreign users.

Alipay Limits for Foreign-Linked Cards

The single transaction limit for foreign users is approximately USD 5,000, with an annual cumulative spending cap of around USD 50,000.

Before these higher limits apply, you may encounter initial tiered limits, such as 3,000 CNY per transaction and 50,000 CNY per month, until you complete additional passport verification in the app.

You can generally spend up to 15,000 CNY without extra verification, but completing your passport ID check is recommended to access higher limits.

WeChat Pay Limits for Foreign-Linked Cards

Common limits are 6,000 CNY per single transaction, 50,000 CNY per month, and 60,000 CNY per year when using an international card.

A key cost factor is the transaction fee: payments under 200 CNY are usually free, while transactions above that threshold incur a cross-border fee of about 3%.

Similar to Alipay, foreign WeChat Pay accounts are primarily for merchant payments and do not support full P2P transfers or features like red packets (hongbao).

Risks and Practical Advice for Business Payments

Paying a supplier’s private personal wallet is often technically impossible or risky due to P2P restrictions on foreign accounts and the lack of formal documentation.

Even if a workaround exists, large transfers to personal accounts can quickly hit your annual cap and raise compliance flags, offering no protection in disputes.

For reliable, high-value payments to factories or booths, use formal methods like bank transfers (T/T) or ensure the supplier can accept card payments through a registered merchant QR code, which stays within platform rules.

Your Direct Line to Yiwu. Save 10%, Avoid the Headache.

Bank Transfer (T/T): Private vs. Company Accounts

Bank transfers (T/T) have distinct characteristics depending on whether you use a private personal account or a company corporate account. The key differences lie in transaction limits, access controls, fee structures, and their suitability for business-scale payments.

Understanding the Core Differences

A private account is designed for individual use, with lower transaction limits and simpler access for one user.

A company account is built for business operations, supporting higher transaction volumes and allowing multiple users with different authorization levels.

The fee structure differs: personal accounts typically have lower maintenance costs, while corporate accounts incur higher fees for specialized services like cash flow tools.

Practical Implications for Sourcing Payments

For business-to-business payments like supplier invoices, a corporate account is essential for compliance, traceability, and handling the required amounts.

Using a private account for a trade deal can be a red flag; suppliers requesting payment to a personal account may indicate a higher risk of fraud.

Recent regulatory updates in markets like the U.S. allow corporate wire transfers of up to $10 million per transaction, facilitating large-scale international payments.

Best Practices and Risk Management

Always verify that a supplier provides a legitimate company bank account for receiving payments to ensure a proper paper trail.

Despite the prevalence of checks, data shows wire transfers could grow significantly with better financial tools, highlighting a shift towards digital B2B payments.

For managing multiple payments to different suppliers, consolidating funds through a trusted sourcing agent can streamline the process and reduce individual wire transfer fees.

The “Frozen Account” Risk Explained

A “frozen account” risk in finance, particularly related to payment methods like credit cards, refers to a credit freeze on your credit report. This protective measure blocks access to your report to prevent fraud but can also hinder legitimate transactions, such as using your credit card at a booth or accessing private personal accounts.

What a Credit Freeze Is and Why It’s Used

A credit freeze, often called a ‘frozen account,’ blocks access to your credit report to prevent new accounts from being opened by identity thieves.

It’s a more powerful tool than a fraud alert, which only requires lenders to verify your identity before approving credit.

Freezes are free, do not affect your credit score, and are the most effective defense against new account fraud, yet only about 10% of consumers use them.

Limitations and Real-World Impact for Importers

A freeze does not protect against fraud on existing accounts, which accounts for 78% of identity theft, so monitoring statements is still essential.

For importers, a freeze can unexpectedly block legitimate transactions, like using a credit card at a supplier’s booth if the payment triggers a credit check.

To make a payment, you must temporarily ‘thaw’ the freeze using a unique PIN provided by each of the three major credit bureaus (Equifax, Experian, TransUnion).

How to Manage a Freeze and Regional Trends

You must contact each credit bureau (Equifax, Experian, TransUnion) separately to place or lift a freeze, a process that requires planning ahead for major financial steps.

Adoption rates vary significantly by state; Colorado leads with 26.5% of consumers using a freeze or alert, while Tennessee has the lowest rate at 6%.

Despite the high risk of identity theft, only 17% of consumers nationwide have any form of credit protection in place, highlighting a significant gap in financial security.

Using a Sourcing Agent for Payment Consolidation

A sourcing agent simplifies cross-border and trade fair payments by acting as a central hub. They collect your funds once and then distribute payments to multiple suppliers, reducing transaction counts and administrative work while improving security and compliance.

What Payment Consolidation Is and How It Works

A sourcing agent acts as an intermediary, combining payments to multiple suppliers or booths into one centralized transaction for the buyer.

This is common at trade fairs or for cross-border sourcing, where the agent collects funds via card, bank transfer, or digital wallets and then disburses them to individual vendors.

The process reduces the number of separate transactions a buyer must manage, simplifying invoicing and financial tracking.

Operational Benefits and On-Site Payment Changes

Consolidation enables card payments at booths where individual vendors lack merchant accounts, as the agent provides a unified POS or QR code system.

It centralizes reconciliation, automatically tagging sales to specific suppliers or booths, which replaces manual spreadsheet tracking with automated reporting.

This workflow significantly reduces administrative overhead for both buyers and event organizers.

Risk Management and Compliance Advantages

Using an agent’s business account for consolidation minimizes the need to pay private personal accounts, which carry higher fraud and regulatory risks.

The agent manages PCI-DSS compliance, fraud monitoring, and chargeback processes centrally, offering clearer dispute resolution for buyers.

This structured approach provides better audit trails, KYC/AML screening, and overall financial security compared to dealing directly with numerous small vendors.

Frequently Asked Questions

Do Yiwu suppliers accept credit cards?

Most Yiwu market suppliers do not accept international credit cards directly at their booths. While a few larger shops might accept UnionPay or international cards, it’s uncommon. Experienced importers typically use bank transfers (T/T), Alibaba Trade Assurance (where you pay Alibaba by card), or pay a sourcing agent who accepts cards and settles with the supplier in CNY. Direct card payments to a supplier’s personal account are rare and carry higher risks.

How do I link a foreign credit card to Alipay?

To link a foreign card to Alipay, download the app, sign up with your international phone number or email, and complete mandatory real-name verification using your passport. Then, go to ‘Bank Cards’ to add your Visa, Mastercard, JCB, Discover, or Diners Club card. The process requires entering your card details, setting a payment password, and verifying the card via an SMS code or a small test charge from your bank. It’s best to set this up before arriving in China to test it with a small purchase.

Is it safe to pay a supplier’s personal bank account?

Paying to a personal bank account increases your risk. While it might be convenient for the supplier, it weakens your legal and financial protections. It’s harder to prove the payment was for a business transaction, complicating disputes or chargebacks. For higher-value orders, it’s safer to pay into a verified company bank account or use a platform with escrow services like Alibaba Trade Assurance to ensure traceability and accountability.

What is the typical exchange rate for payments?

There isn’t a single ‘market’ rate. When paying by international credit card, the effective cost includes the network’s interchange fee (typically 1-3% of the transaction) plus any foreign transaction fees from your bank. These fees vary by card network, region, and transaction type. For bank transfers (T/T), you’ll get the wholesale exchange rate from your bank, which is usually better than dynamic currency conversion offered at point-of-sale. Always confirm the final amount you will pay in your home currency, including all fees.

Can I pay in RMB cash in Yiwu?

Yes, you can pay in RMB cash, and it is widely accepted at Yiwu market booths, often alongside mobile payments. It’s a reliable backup, especially for smaller purchases. However, carrying large amounts of cash has security risks. For larger orders, suppliers typically expect a bank transfer. You can obtain RMB by exchanging currency at banks or using ATMs with your international card; try to get smaller denomination bills (like ¥10, ¥50) for easier transactions.

Final Thoughts

Choosing the right payment method in Yiwu depends on your order size, risk tolerance, and the supplier’s setup. For small, in-person purchases, RMB cash or a foreign-linked Alipay/WeChat Pay account works well. For serious business orders, a bank transfer (T/T) to the supplier’s verified company account is the standard, safest route. Avoid using personal accounts or trying to force peer-to-peer mobile payments for large amounts.

The most efficient approach for many importers, especially when dealing with multiple suppliers or visiting trade fairs, is to work with a sourcing agent. They consolidate payments, handle local currency transactions, and provide a secure bridge between your international funds and the suppliers’ expectations. This simplifies logistics and significantly reduces the payment risks outlined here.